If you are afraid just by the thought of unending paperwork and record entries which is preventing you from getting a Home Loan, stress no more! Presently getting your fantasy home is never again an overwhelming errand, check your qualification, analyze between various banks, and apply for a Home Loan that best suits your requirements.

There is a ‘Ladies’ Special’ offering as well. This advance is accessible if the essential candidate is a lady or the main co-candidate (in the event of a joint application) is a lady. This advance additionally doesn’t require any printed material and has comparative highlights to the credit talked about above. The main contrast is that the loan cost begins from 8.35%. Intrigued?

You, for the most part, take a home loan for either purchasing a house/level or a plot of land for development of a house, or redesign, augmentation, and repairs to your current house.

FOLLOWING QUESTIONS WILL ANSWER ALL YOUR QUERIES

What amount of home loan am I qualified for?

Before you begin the home loan process, decide your aggregate qualification, which will basically rely on your reimbursing limit. Your reimbursement limit depends on your month to month dispensable/surplus salary, which, thusly, depends on variables, for example, add up to month to month pay/surplus less month to month costs, and different elements like life partner’s pay, resources, liabilities, security of wage, and so on.

The bank needs to ensure that you’re ready to reimburse the advance on time. The higher the month to month extra cash, the higher will be the credit sum you will be qualified for. Commonly, a bank expects that around half of your month to month dispensable/surplus pay is accessible for reimbursement. The residency and financing cost will likewise decide the credit sum. Further, the banks, for the most part, settle an upper age constraint for home advance candidates, which could affect one’s qualification.

What is the extreme sum I can obtain?

Most banks require 10-20% of the home’s price tag as an initial installment from you. It is additionally called ‘one’s own particular commitment’ by a few banks. The rest, which is 80-90% of the property estimation, is financed by the loan specialist. The aggregate financed sum likewise incorporates enrollment, exchange, and stamp obligation charges.

Despite the fact that the loan specialist computes a higher qualified sum, it isn’t important to get that sum. Indeed, even a lesser sum can be acquired. One should attempt to organize the most extreme of initial installment sum and less of home loan with the goal that the intrigue cost is kept at negligible.

Is a co-candidate important for a home loan?

Truly, it is (for the most part) required to have a co-candidate. If somebody is the co-proprietor of the property being referred to, it is important that he/she additionally be the co-candidate for the home advance. On the off chance that you are the sole proprietor of the property, any individual from your close family can be your co-candidate.

What legal documents, for the most part, are looked for advance approval?

The credit application frame gives an agenda of records to be joined to it, alongside a photo. Notwithstanding all the authoritative reports identified with the buy of the house, the bank will likewise request that you present your personality and home confirmations, most recent compensation slip (verified by the business and self-bore witness to by you) and Form 16 or wage expense form (for agents/independently employed) and the most recent a half year bank proclamations/monetary record, as relevant. A few loan specialists may likewise require guarantee security like the task of extra security arrangements, the vow of offers, national reserve funds endorsements, common store units, bank stores or different speculations.

What is accredited and installment of a loan?

In view of the narrative evidence, the bank chooses whether or not the advance can be endorsed or given to you. The quantum of the credit that can be authorized relies upon this. The bank will give you an authorization letter expressing the credit sum, residency, and the financing cost, among different terms of the home advance. The expressed terms will be legitimate until the point that the date specified in that letter.

At the point when the advance is really given over to you, it adds up to dispensing of the advance. This happens once the bank is through directing specialized, legitimate and valuation works out. One may settle on a lower credit sum amid dispensing against what is said in the endorse letter. At the disbursal arrange, you have to present the portion letter, photocopies of title deed, encumbrance authentication and the consent to offer papers. The loan fee on the date of dispensing will apply, and not the one according to the endorse letter. In such a case, another authorize letter gets readied.

In what manner will the payment happen?

The advance can be dispensed in full or in portions, which generally does not surpass three in number. In the event of an underdevelopment property, the payment is in portions in view of the advance of development, as surveyed by the loan specialist and not really as indicated by the designer’s understanding. Make a point to go into a concurrence with the engineer wherein the installments are connected to the development work and not pre-characterized on a period based calendar. If there should arise an occurrence of a completely developed property, the payment is made in full.

What are the loan fee alternatives?

Home loan rates can be either settled or adaptable. In the previous, the financing cost is settled for the credit’s whole tenor, while in the last mentioned; the rate does not stay settled.

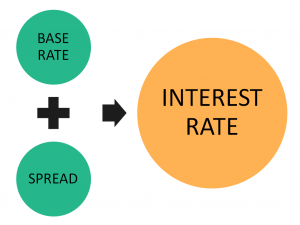

What is the minimal cost of assets based loaning rate (MCLR)?

Another strategy for bank loaning called minor cost of assets based loaning rate (MCLR) was set up for all advances, including home advances, after April 1, 2016. Prior, credits were connected to the bank’s base rate. While new borrowers after April 1, 2016, can just take MCLR-connected advances, the borrowers on the base rate have the alternative to change to MCLR.

Under the MCLR mode, the banks need to survey and announce overnight, one month, three months, a half year, one-year, two-year, three-year MCLR rates every month. The real loaning rates are dictated by adding the segments of spread to the MCLR. So a save money with a 1-year MCLR of 8% may keep a spread of 0.5%, in this way the genuine loaning rate ends up 8.5%.

Banks may determine premium reset dates on their coasting rate credits and at present have a year reset proviso. The periodicity of reset is one year or lower. The MCLR winning on the day the advance is endorsed will be pertinent till the following reset date, independent of the adjustments in the benchmark amid the between time period.

For most MCLR-connected home loan gets, the banks reset the loan fee following a year. So on the off chance that somebody has taken a home advance from a bank, say, in May 2016, the following reset date will be in May 2017. Any modifications by the Reserve Bank of India (RBI) or the banks won’t affect compared regularly scheduled payments (EMIs) or the credit.

In a falling loan fee situation, quarterly or half-yearly reset choice is better, given the bank concurs. However, when the loan fee cycle turns, the borrower will be off guard. Subsequent to moving to the MCLR framework, there is dependably the danger of any upward development of financing costs before you achieve the reset time frame. On the off chance that the RBI raises repo rates, MCLR, as well, will climb.

What is base rate and what do you do if your home loan is connected to it?

All rupee advances endorsed and credit limits reestablished after July 1, 2010 (yet before April 1, 2016) are estimated with reference to the base rate. There can be just a single base rate for each bank. Under it, banks have the opportunity to compute the cost of assets either based by and large cost of assets or on the negligible cost of assets.

Post-MCLR, the current credits connected to the base rate may proceed till reimbursement or reestablishment, all things considered. Existing borrowers will likewise have the choice to move to the MCLR-connected advance at commonly worthy terms.

Your Home Loan is connected to the base rate.

One reason could be that your Home Loan rate is connected to bank’s base rate and not the Marginal Cost of Lending Rate (MCLR). Base rates are not reset as regularly as the MCLR. This could why your credit rate is still high.

Consider changing to an MCLR-based Home Loan. Just banks offer MCLR-based advances while Non-Banking Finance Companies have Primer Lending Rate (PLR) which is like base rate. Despite the fact that MCLR-based advances are not precisely the purest type of drifting rate credits, they will be reset by banks more regularly than base-rate advances. When the MCLR is reset on the reset date, you can appreciate bring down financing costs on your credit.

How does the reset happen? On the MCLR reset date, the loan fees in the nation as on that date will be utilized for resetting. Likewise, MCLR is normally reset when the Reserve Bank of India (RBI) changes the loan fees. Banks will charge you for changing your credit to the MCLR-based advance. This could be anyplace between 0.2%-0.5% of your remarkable advance sum.

Your bank isn’t giving the best interest rates?

At times your moneylender may very well not give you bring down rates either in light of the fact that you have a settled rate advance and are not qualified for bringing down rates or in light of the fact that your loan specialist has no plans to bring down rates whenever later on.

The ideal route forward is to pick MCLR-based credit suppliers with the briefest conceivable MCLR to reset dates. While a few banks reset MCLR once in a year, there are banks that reset MCLR on a half-yearly premise. The shorter the MCLR reset date, the better for you as long as the financing cost is falling.

In any case, before you change to another bank, you should do some money saving advantage examination. This will let you know whether it bodes well to really change to another loan specialist. For this, you should figure the cost of the advance exchange and the new EMI to see if it is justified regardless of all that issue. Credit expenses will incorporate preparing expenses, stamp obligation charges, legitimate charges and valuation charges, among others. How huge could this sum be? At times this can be as much as 5% of your credit sum. Along these lines, check the amount you will spare in enthusiasm by changing to another moneylender before you choose to switch.

Home Loan rates now are as low as 8.3%. Along these lines, simply ahead and get that Home Loan immediately. We will enable you to contrast crosswise over banks with getting the advance that is ideal for you.

Can I get a home improvement loan if I already have a home loan?

A home improvement loan is offered to encourage the change of a self-claimed property to existing or new clients. This advance might be utilized for repairs, remodels, change, and expansion of the house. The advance works this way: The borrower should work out a cost gauge of the work proposed to be done and offer it to the bank, who will take a citation from the contractual worker to confirm the gauge submitted. The cash is discharged at the rate of the development work to the temporary worker to confirm the gauge submitted. The cash is discharged at the rate of the development work to the temporary worker to whom it is expected.

What do you do in the event that you have a complaint?

In the event that you have a protestation against a planned bank, you can stop it with the concerned bank in writing in a particular dissension enlist gave at the branches. Request a receipt of your protestation. The points of interest of the authority accepting your protest might be particularly looked for.

The grievance can likewise be held up by your approved delegate (other than a legal counselor) or by a purchaser affiliation/discussion following up for your benefit. On the off chance that you are miserable with the Ombudsman’s choice, you can engage the Appellate Authority in the RBI.